Concerns about the Omicron variant raised the risk of additional lockdowns and contributed to a decline of more than 2% in the S&P 500 on the day after Thanksgiving. The COVID-19 variant, first detected in South Africa, triggered travel restrictions in the U.S. and Europe.

Key Points for the Week

- New cases of the Omicron variant are being discovered, and concerns about renewed social distancing pushed markets lower on Friday.

- Core inflation rose 0.4% last month and has climbed 4.1% in the last year, according to the Federal Reserve’s preferred measure of inflation.

- The number of cargo ships waiting to unload at Southern California’s main port has dropped by 45% in the last two weeks, indicating shipping challenges are continuing to improve.

Other data points provided a mixed picture. Energy and automobile prices shot higher and contributed to inflation increasing 0.6% based on the personal consumption expenditures (PCE) price deflator. Large price jumps for gasoline and automobiles contributed to the increase. Stripping out the volatile food and energy components lower the increase to 0.4% in October and 4.1% during the last year.

Supply chain challenges, which have contributed to higher inflation, seem to be improving. The number of cargo ships waiting to unload at either Los Angeles or Long Beach harbors dropped from 111 to 61 in the last two weeks. Supply chain issues have slowed housing construction. Approximately 36% of new homes have been purchased but construction has yet to be started.

The S&P 500 index sagged 2.2% last week. The MSCI ACWI fell 2.8%. The Bloomberg U.S. Aggregate Bond Index also dropped 0.3% last week. The October employment report and news about the Omicron variant will be at the top of our list to monitor this week.

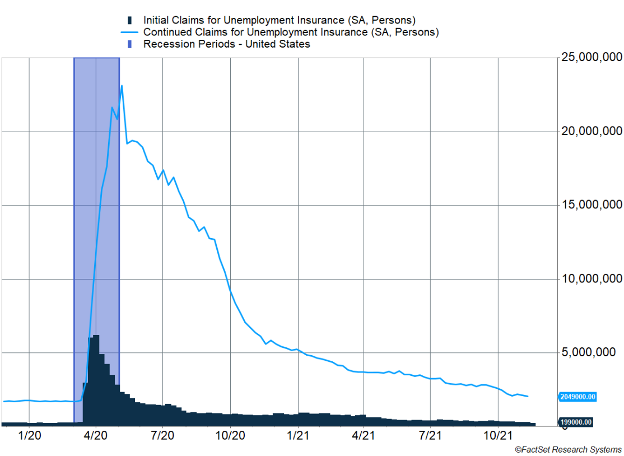

Figure 1

Risk #1 is Back

At the beginning of each quarter, we identify five big risks to watch. Virus variants have been the top risk for many quarters in a row. Unfortunately, it looks like Risk #1 is about to reassert itself. The Omicron variant was discovered in South Africa, and other cases have popped up in other parts of Africa and Europe. Some experts believe the variant may have developed elsewhere in Africa and then transferred to South Africa.

Our concern has always been a more contagious variant that renders vaccines less effective could push economies back into lockdown. It is not yet known whether Omicron causes more severe illness or is vaccine resistant, but medical experts are concerned the high number of mutations compared to previous variants will cause it spread even more rapidly than Delta.

Even if the Omicron variant spreads rapidly, the economic and market impact is unlikely to be as severe as the first COVID wave. Countries and companies have proven an ability to adjust to lockdowns and find ways to maximize output while reducing spread and interaction. The U.S. and many European countries banned travel from South Africa and some other African countries to help contain the variant.

The resurgence of virus risk comes as other top risks were also making news. The presidents of China (Risk #2) and the U.S. held a call to smooth out differences. Early signs indicated supply chain difficulties (Risk #4) may be easing. The number of containers left at the docks in Long Beach and Los Angeles, which account for about 40% of freight entering the U.S., decreased by 33% in the last two weeks.

Hiring also continues to improve. U.S. first-time jobless claims fell to their lowest level in 52 years, dropping to 199,000 for the first time since 1969. Initial claims have been steadily decreasing since an uptick in September when fears of the Delta variant peaked. Initial claims have now dropped below the 2019 average of 218,000 (Figure 1). This data is further evidence that the U.S. labor market is continuing to recover from policy decisions (Risk #3) that helped push some people out of the workforce.

The emergence of a new variant and the good news on the supply chain and jobs reinforce our view that we should remain risk-aware but optimistic. In many ways, investor behavior (Risk #5) is the risk we control the most and analyze the least. Just because the S&P 500 hadn’t dropped more than 1% since early October didn’t mean it couldn’t at any time. Don’t be surprised if markets get more volatile as they quickly adjust in price to reflect new information. Likewise, look for supposedly intractable problems to potentially be solved by the steady effort and innovation of capitalist economies.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.dol.gov/ui/data.pdf

https://www.bea.gov/news/2021/personal-income-and-outlays-october-2021

Compliance Case # 01196877